In Citi's Steven Englander's latest note, he notes that *every major FX trade in place right now is a carry trade in one form or another, differing only in their scope and in the risk they entail*. This has 5 significant implications...

In Citi's Steven Englander's latest note, he notes that *every major FX trade in place right now is a carry trade in one form or another, differing only in their scope and in the risk they entail*. This has 5 significant implications...Via Citi,

This note argues that every major FX trade in place right now is a carry trade in one form or another, differing only in their scope and in the risk they entail. Consider the following trades that encompass the vast majority of FX trades in place:

1) In Asia, long CNH, short USD

2) In G3, long USD, short EUR and JPY

3) In G10 long AUD and NZD, short G3

4) Globally, long EM, short G3

In the short term, we think *2) remains the most robust because acutely disappointing economic outcomes will likely induce ECB and BoJ action*. If anything, FX moves are lagging moves in vol-adjusted carry. Fear of more aggressive Fed tightening is the likely driver of higher volatility but this would push spreads further in favor of the USD, offsetting some of the impact of higher volatility. Hence, these carry trades are not as vulnerable as 3) or 4) to Fed-induced volatility. However, we saw earlier this year that long USD against EUR and JPY is sensitive to generalized position unwinds, at least temporarily.

*On a 2-4 month horizon 3) and 4) are the most vulnerable* because we expect investors to become much less certain that the Fed pricing pace will be as shallow as the market now expects (link), and they would be hit doubly by any backing up of volatility. We look to payrolls and FOMC this week and next as potential triggers for an unwind of these trades, but we think there will be more sensitivity once QE is ended and the unemployment rate falls below 6% -- most likely in early November.

*Five implications:*

a. Yield advantage is the driver in all these trades, and the yield advantage is often at multi-year highs when adjusted for volatility

b. *All these trades have enormous sensitivity to a run-up in asset market volatility* (except possibly 1)

c. Long high-beta EM and long AUD, NZD in G3 trades suffer the most on a vol spike

d. EM currencies have further to fall against USD than EUR and JPY to rise against USD in the event of a vol spike

e. *The trades are all highly dependent on policymaker intentions* – 1) depends on Chinese policymaker tolerance of CNH appreciation and positioning, 2) on explicit easing measures by the ECB and BoJ, 3) and 4) exist only if the Fed normalization path is extremely shallow.

*The Trades in detail...*

*1) Long CNH, short USD*

The baby carry trade is in Asia, where the perceived low-risk, low-return carry trade is long CNH, short USD. During my recent Asia visit this was by far the most prevalent trade held by investors and seems to be the default trade for those uncomfortable with EM or G3.

Figure 1 shows the 3-mth CNY less USD rate differential, divided by USDCNH 3-mth implied vol. This ratio exceeds 1 and is hard to resist when vol-adjusted rate differentials in G10 are typically far less than 0.5. Moreover, Asian investors feel that Chinese policymakers remain committed to providing stimulus and will not shock investors by pushing the CNY fix in the opposite directions.

*2) Long USD, short EUR and JPY*

The G3 version of the carry trade is long USD, short EUR or JPY. In Figure 2 we see the US minus japan, 10year yield differential adjusted for USDJPY implied volatility. Note the spike in vol-adjusted carry earlier this year. Even with a pullback from the peak, the current vol-adjusted yield differential is the highest since 2007. The last time the vol adjusted yield differential was this wide, USDJPY was trading in a 110-115 range so there is still some room for JPY weakness, and even more if US yields begin to back up while Japanese yields stay in place.

Embedded in the recent JPY weakness is some expectation that the BoJ will ease policy. With JGB yields almost at all-time lows and JPY under pressure, it looks as if investors are more focused on the BoJ than cancellation of the second sales tax hike. The current level of Citi’s Economic Surprise Index for Japan is at a lower level than at the worst in 2008-2009 (Figure 3).

The ESI is mean reverting almost by construction (it would take an accelerating death spiral in an economy to make the ESI non-stationary). That does not mean that every move is equivalent. The ESI could increase because economic performance outstrips expectations, which presumably would be a JPY positive. It could also increase because expectations dropped sufficiently to match continuing dismal performance. That downward revision to expectations would probably be JPY negative.

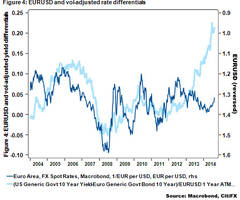

On the EUR side, vol-adjusted rate differentials are at their highest in 15 years. Moreover, based on the relationships of the last few years, the current vol-adjusted yield spread looks consistent with EURUSD at parity (Figure 4). Moreover, even the convergence trade has disappeared – only Italy, Greece, Portugal and Slovenia 10-yr sovereign yields are higher than in the US, and for Italy only by a couple of basis points.

Bottom line is that there is a mini-carry trade within G3 that is driving USD against EUR and JPY. It is policy dependent because further policy moves are probably 40-50% priced into JPY and EUR yields, but the trade remains attractive because the EUR and BoJ are increasingly likely to ease further and the risk on the Fed is that it surprises on the aggressive side.

*3) and 4) Long high-beta carry, short G3*

CitiFX’ s positioning indicator (Figure 5) provides a good summary of the state of positioning play: i) long USD, but primarily versus G10; ii) long EM; iii) long commodity currencies (green); iv) long APAC and High Yield (purple); v) short G5 ex US.

Figure 6 gives an indication of why investors are so enthusiastic about EM and high yielders in general. Vol-adjusted spreads for Brazil and South Africa are close to the post-2007 highs. Vol-adjusted spreads for NZD are at similar highs, but at far lower levels, comparable to USD vs. EUR. By contrast vol-adjusted spreads for Australia versus the US are at the low end of recent experience, so there may be some sensitivity if Australian data weaken.

* * *

Isn't everything the same trade now? Reported by Zero Hedge 2 hours ago.