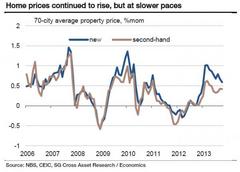

The only numbers that matter today are 16000, 4000 and 1800: those are the Fed's closing targets for the Dow Jones, the Nasdaq and the S&P. Following last night's Chinese euphoria which saw the Shanghai Composite surge by 2.87%, or up 61.4 to just under 2,200 on renewed hopes for Chinese reform by 2020, the Fed's price targets should all be quite easily achievable. And not even the rising home prices in 69 out of 70 cities year over year, and 65 over month - the same as last month, with new nome price inflation at 0.6% overall and 0.8% for the first tier cities, was able to put a dent in the reflationary spirits in the Mainland. Additionally, news that China would join the US and Europe in "adjusting" its GDP calculation method, which would add R&D expensing into the bottom line, and as a result boost the overall number, is, well, helping things.

The only numbers that matter today are 16000, 4000 and 1800: those are the Fed's closing targets for the Dow Jones, the Nasdaq and the S&P. Following last night's Chinese euphoria which saw the Shanghai Composite surge by 2.87%, or up 61.4 to just under 2,200 on renewed hopes for Chinese reform by 2020, the Fed's price targets should all be quite easily achievable. And not even the rising home prices in 69 out of 70 cities year over year, and 65 over month - the same as last month, with new nome price inflation at 0.6% overall and 0.8% for the first tier cities, was able to put a dent in the reflationary spirits in the Mainland. Additionally, news that China would join the US and Europe in "adjusting" its GDP calculation method, which would add R&D expensing into the bottom line, and as a result boost the overall number, is, well, helping things.Finally, with today's POMO a rather whopping $3-$4 billion, it is only a matter of time before all three of the previously noted psychological resistances are promptly taken out by the Fed's open markets desk.

Not much on deck today, aside from more speeches from Dudley, Plosser and Kocherlakota which will incite even more multiple expansion.

*US reports:*

· US: NAHB housing market index, cons 56 (10:00)

· US: sells $32bn 3m and $28bbn 6m bills (11:30)

· US: Fed speakers Dudley (12:15 and 15:45), Plosser (13:30)

*Market Re-Cap from RanSquawk

*

Stocks in Europe this morning trade relatively higher with the FTSE MIB leading the way this morning with Italian Banks including Banco Popolare providing upward momentum for Italian equities. Following the positive sentiment observed across Asia overnight, the German DAX has managed to print an all time high above the 9200 level. In terms of underperforming indices the FTSE-100 is being weighed down by Petrofac who are trading with significant losses this morning following reports that the company expected group net income in 2014 to show flat to modest growth Y/Y. However, the FTSE-100 is being supported by Aberdeen Asset management following reports that Lloyds are to sell asset management SWIP for about GBP 560mln. In terms of sector performance, utilities are leading the way after RWE were upgraded to outperform vs neutral at Exane.

From a fixed income perspective, markets are struggling to find direction with little in the way of news flow and volumes coming out of this morning’s quiet session. In terms of FX markets, overnight AUD gained and broke above the 0.9400 level as markets reacted positively to the release of Friday’s Chinese Plenum reform document which saw stocks rally overnight. Furthermore, market participants will be keeping an eye on EUR/USD which is trading in close proximity to an option expiry at 1.3500.

Looking ahead for the session there is little in the way of tier-1 data for the session. However, there are a few scheduled speakers which includes the likes of Fed’s Dudley and Plosser after-market.

*Overnight bulletin summary from Bloomberg and RanSquawk:*

· The Shanghai Composite finished with gains of 2.9% as markets had their first chance to react to Friday's Chinese Plenum document release. Furthermore, The Chinese National Bureau of Statistics is planning to change the way it calculates GDP to reflect changes in international standards which should see a boost to GDP readings.

· Stocks in Europe reacted positively to the news with the German DAX printing an all-time high above the 9200 level.

· Treasuries steady, 10Y at 2.70% holding just above 50-DMA at 2.677% before speeches from Dudley and Plosser after Yellen last week signaled ongoing easing.

· ECB Executive Board member Yves Mersch said risk scenarios in upcoming stress tests on bank balance sheets are likely to use 2016 as their end-point

· Defaults as a proportion of total lending at Spanish banks increased to a record in September as more borrowers missed loan payments in an economy with unemployment at 26%

· Obama pressed top U.S. insurers to help consumers cope with the rocky start of his health-care law as the House passed a bill that would let Americans keep their current policies through 2014; 39 Democrats supported the Republican bill

· Sovereign yields mostly higher, EU peripheral spreads mixed. Shanghai Composite surges nearly 3%; European stocks, U.S. equity-index futures higher. WTI crude, copper and gold lower

*Asian Headlines*

The Chinese National Bureau of Statistics is planning to change the way it calculates GDP to reflect changes in international standards according to Xu Xianquan, Deputy Heads of the NBS. The new method may boost Chinese GDP. This saw the Shanghai Composite, finish with gains of 2.9% at 2,197.22

Japan’s USD 1.2trl public pension fund should be remade as a new, independent entity, a panel tasked with proposing an overhaul of the fund are likely to recommend. The move could unleash a flood of cash into global markets and change the way trillions of JPY is invested. As a guide, a 1ppt move in the allocation to domestic stocks could send JPY 1.2trl into the market.

*EU & UK Headlines*

ECB’s Coene (dove, Belgian) does not see the need for more rate cuts.

ECB's Praet (neutral - executive board, Belgian) said that should interest rates be lowered to zero, ECB could still deploy quantitative measures, including buying government bonds, or injecting capital into banks; but added that “we are not at this point”.

German finance minister Schaeuble said Germany will not face sanctions on trade surplus.

ECB's Nowotny says that the ECB still has measures to fight low inflation if needed.

Eurozone Current Account NSA (Sep) M/M 14.0bln vs. Prev. 12.0bln (Rev. 12.4bln)

Current Account SA (Sep) M/M 13.7bln v. Prev. 17.4bln (Rev. 17.9bln)

*US Headlines*

According to the FT Obama's Presidency is not over but is failing, saying that with the exception of the debt ceiling, he has fallen at almost every hurdle.

After opening lower amid touted profit taking from last weeks significant gains, stocks across Europe are now trading mostly in the green with the FTSE MIB leading the way following strong performances from Italian banks. Of note, Aberdeen Asset management are helping prop up the FTSE 100 and halt the downward pressure being exerted on the indicie with Petrofac currently down around 14% following company expected group net income in 2014 to show flat to modest growth Y/Y. Furthermore the German DAX has printed record highs in this mornings trade above the 9200 level.

*FX*

In FX markets, overnight, AUD managed to gain from the positive sentiment from the Asian session and NZD saw upside following New Zealand PMI (Oct) M/M 58.2 vs. Prev. 55.6 (Prev. 56.4) - highest since November 2007. This morning much of the movement across the market is being observed as a result of EUR/USD which is currently heading towards a touted option expiry at 1.3500. Markets will also be keeping an eye of EUR/GBP with market talk of offers mooted at 0.8390 with stops tipped above 0.8400. With little left in the session in terms of macroeconomic data releases, markets may be looking ahead to any comments from Fed's Dudley and Plosser.

*Commodities*

Heading into the North American open, WTI crude and brent futures trade in minor negative territory with WTI crude futures falling after data from the Join Organisations Data Initiative showed that Saudi Arabia exported more oil in September than in any month since November 2005. Furthermore, prices have seen further downside following reports that Russian President Putin believes there is a real chance to resolve the dispute over Iran's nuclear programme.

Citigroup have reduced their Brent price forecast amid a growing bullish outlook with the bank forecasting Q4 Brent at USD 105 per barrel and USD 98 per barrel by 2014.

Libya has resumed gas exports to Italy after protesters left the North African country's Mellitah port, and expects to begin loading condensate there on today according to the the NOC. Elsewhere, the Oil Ministry says Ras Lanuf is Libya's only refinery still shut.

*SocGen's summarizes the main macro events of the day:*

Risk assets gave the thumbs up to Janet Yellen's testimony by pushing the S&P into unchartered territory, and the index now sits within striking distance of 1,800 having marked an 8% gain over the past month. US 10y yields and swaps have gone up a puny 3bp over the same period, and the broad dollar index has gained just 0.6% (0.4% vs the EUR and 1.6% vs the JPY). The S&P beats Eurostoxx hands down (the latter having rallied only 5.8%), from which we can infer that because of the resilience of the EUR and the negative impact on corporate profits, investors are more reluctant to invest in the euro area. However, the flip side is that falling inflation and a dovish ECB are turning euro-area debt into a more attractive proposition than US debt, though weak nominal growth may dampen some of the enthusiasm. Even if Fed tapering is delayed until March 2014, the prospect of higher yields is greater in the US (and the UK) than it is in the eurozone.

Nothing stands in the way of the US Senate formally completing the nomination of Janet Yellen, and a vote planned for this week will ensure that the handover happens after the January FOMC meeting. The immediate focus for the rates and FX markets is the minutes of the October FOMC meeting this Wednesday. Yellen's testimony did not suggest that tapering is imminent, but details of the discussions will be scrutinised for any hint that asset purchases could be reduced earlier than March.

The advance eurozone PMIs and the German ZEW survey will attract most of the interest this week, with investors on the lookout for an update on growth momentum in Q4. Spain and Italy were singled out on Friday by the European Commission under its new budgetary surveillance exercise, and it warned that the 2014 budget plans for both countries are at risk of not complying with new debt and deficit rules (link). The forecasts approved by the Spanish parliament envision a budget deficit of 5.9% of GDP in 2014 and 6.6% in 2015, well above the EU-mandated 3% threshold for 2016, but the EC's observations could well entail fresh spending cuts and a delayed strengthening of domestic demand.

In EM, the South African Reserve Bank is expected to keep its benchmark rate unchanged at 5.0% this Thursday. With headline inflation running at 6% and the ZAR having lost 4% vs the USD since the September meeting, will the SARB take a more hawkish policy line? USD/ZAR and EUR/ZAR have started to retrace from overbought levels, but the case of Indonesia last week demonstrated that raising rates is not the silver bullet that will stop the currency depreciating.

*DB's Jim Reid complete the overnight recap:*

Can China be the best it can be going forward? Well markets are this morning more positive on the additional details released on Friday night from China’s Third Plenary Meeting that ended early last week. This has been better received than last week’s official post-meeting communiqué. Asian equities are enjoying robust gains this morning led by the Hang Seng China Enterprises Index (+5.2%), which was also up 3.0% on Friday as talk of the release of the reform details gathered steam. There is hope among analysts that the reforms will mark a turnaround for Chinese equities which have been one of the underperforming bourses this year (Year to date performance: HSCEI –-1.6%, Shanghai Comp –1.9%) and which have lost between 15-30% of their value since 2009. Indeed there has been a fairly strong grab for Chinese equity assets from offshore investors overnight, as evidenced by the fact that a number of offshore A-share ETFs are now trading at a premium to NAV, whereas they have been generally trading at a discount in recent history. Other Asian equity bourses are up between 1-2% overnight. The story in other Chinese-growth related assets are mixed though including copper which is down -0.1% and Australian mining shares – perhaps due to the fact that the reform packages also emphasise a reduction in overcapacity which has affected some parts of the Chinese economy to-date. The Shanghai Composite is up a relatively muted 1.8%.

Going into further detail, China’s reform package was officially titled “Decision on Major Issues Concerning Comprehensively Deepening Reforms”, and was issued on Friday, a few days after the conclusion of “The 3rd Plenum of China’s Communist Party’s (CCP) 18th Congress”. The reform package includes 60 measures. Within these, DB’s Chief Chinese economist Jun Ma believes reforms related to deregulation, opening up of industries, fiscal, financial liberalisation, land and hukou, resource pricing, SOE, social security, two-child policy will have the most profound economic implications. Jun describes the “Decision” as having met 100% of his already extremely bullish expectations and are by far the most profound reforms in a decade, if not decades, in terms of scope, depth, and impact. Indeed, in areas such as SOE and pension reforms the aggressiveness of the reform package surprised him. Jun estimates that relative to the “no-reform” scenario, deregulation will boost the average annual real output growth of the private sector by 3ppts per year in the coming decade. Given these reform benefits, as well as his view that China will experience a cyclical recovery in 2014, our China team expect 20-25% potential upside to MSCI China in the coming 12 months from its current level.

So what’s missing from these reforms? Our view is that while these reforms are a step in the right direction, the difficulty will be in the implementation given there are interest groups in government and in the state-owned sector which will be resistant to change. Some have criticised the reforms as not going far enough on political reforms. Others have suggested that the reforms do not directly address Bank NPLs. On this point, DB’s Jun Ma notes that under the reform plan, the government will permit local governments to issue municipal bonds independently to gradually replace current local government financing mechanisms. Jun argues this will remove a major overhang on bank’s asset quality. This is clearly an evolving story, but one which will have a large ripple effect across DM and EM in the months and years to come. The

proof will be in the implementation. With the weekend newsflow elsewhere relatively quiet, it won't be too long before we get back to US monetary policy headlines. Indeed there are plenty of Fed speakers to listen to this week starting with Bernanke’s Economists Club speech tomorrow and the October FOMC meeting minutes on

Wednesday. Regarding the FOMC minutes, markets will be scanning for clues on the timing of tapering and whether there is anything on strengthening forward guidance. The other key Fed speakers to watch this week are the Philly Fed’s Plosser (today), the Chicago Fed’s Evans (tomorrow), the NY Fed’s Dudley and St. Louis Fed’s Bullard (Wednesday) and Richmond Fed President Lacker (Thursday). This week’s data releases include the NAHB housing market index later today, followed by CPI, retail sales and existing home sales on Wednesday. On Thursday, we have PPI and the Philadelphia Fed survey. A number of US retailers report earnings on Thursday, which should provide further detail on holiday trading outlooks.

Across the Atlantic, Draghi’s speech in Berlin on Thursday will of some interest given the recent talk of the provision of additional liquidity across the euroarea, potentially in the form of asset purchases. The ECB's Weidmann, Noyer, Praet and Nowotny are also set to speak this week. In terms of Eurozone data, watch for the ZEW survey tomorrow, flash PMIs and consumer confidence on Thursday. German trade and the IFO survey round out the weekly data docket on Friday. The BoE’s monetary policy meeting minutes are scheduled for release on Wednesday. In Asia, the BoJ meeting and China’s HSBC flash manufacturing PMI scheduled on Thursday are the main highlights. Reported by Zero Hedge 8 hours ago.